🧾 Social Security's Bitcoin Breakeven

FIRE BTC Issue #81 - The bigger check is probably not worth the wait.

When should I take Social Security?

I've gotten this question a few times now.

The standard answer is usually some version of "delay if you can." Claiming at 62 gives you a smaller check. Waiting until 70 gives you a bigger one. So the traditional planning conversation turns into a breakeven calculation: how long do you need to live before the larger age-70 check makes up for the eight years of payments you skipped?

That's a useful calculation, but I don't think it answers the full question for a financially independent bitcoiner.

If Social Security is income you need to keep the lights on, the claiming decision is mostly about guaranteed cash flow. But if you already have enough portfolio assets to retire, the age-62 check is more than a smaller government benefit. It's cash flow you can control eight years earlier. It can buy bitcoin, or it can let your existing bitcoin and stocks stay untouched while they keep compounding.

So I want to compare two different things. The normal advice compares checks. I want to compare balance sheets.

🏦 The Normal Breakeven

Before we get into the bitcoin angle, it is worth dealing with the standard Social Security argument.

People have been saying for a long time that Social Security will be gone before they ever get to claim it. I don't buy that. Social Security is too embedded in the American psyche, and too politically important, to simply vanish.

That said, the funding problem isn't imaginary.

According to the 2025 Social Security Trustees summary, the Old-Age and Survivors Insurance (OASI) Trust Fund, which pays retirement and survivor benefits, is projected to pay full scheduled benefits until 2033. After that, 77% of scheduled OASI benefits would be payable at reserve depletion. The combined OASI and Disability Insurance (DI) trust funds are projected to deplete in 2034, with 81% of scheduled benefits payable at that time.

In other words, "Social Security will go bankrupt" is too sloppy. The more accurate concern is that future checks may have less purchasing power than people expect. That matters, but it's a different argument than saying the benefit goes to zero.

For now, let's use the current claiming rules.

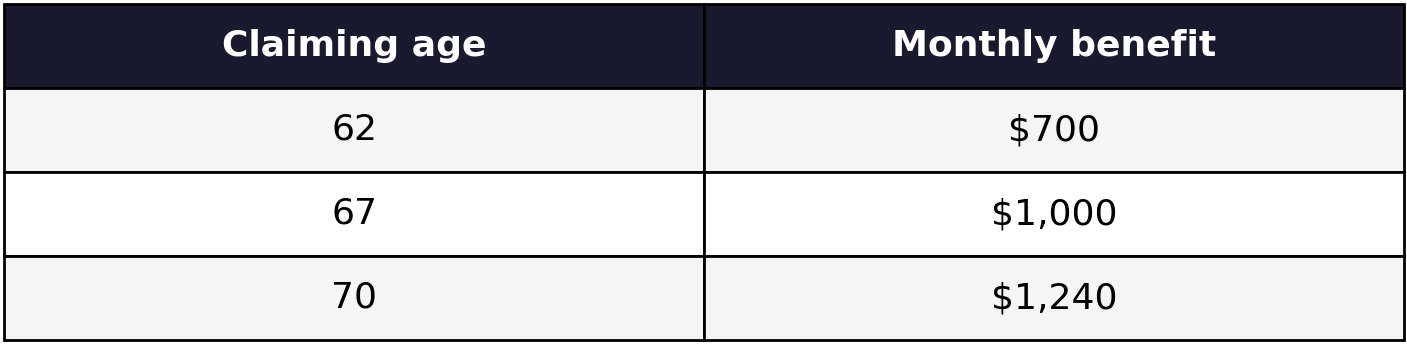

For someone born in 1960 or later, full retirement age is 67. The SSA early retirement table says a $1,000 full-retirement-age benefit would be reduced to $700 at age 62. The SSA delayed retirement credit table says people born in 1943 or later earn delayed credits of 8% per year after full retirement age, up to age 70.

That gives us a simple comparison:

The age-70 check is about 77% larger than the age-62 check. Annualized over the eight years from 62 to 70, that works out to roughly 7.4% per year before cost-of-living adjustments (COLA).

One detail matters here: the delayed credits stop at 70. After that, the age-70 check can still receive cost-of-living adjustments, but it doesn't keep compounding at 8% a year. The age-70 check is larger, but once both people are claiming, it stops pulling away because of delayed-retirement credits.

That sounds pretty good. A guaranteed 7.4% annual increase in a government benefit is nothing to sneeze at.

But there is a cost.

If you wait until 70, you give up eight years of checks. In this example, claiming at 62 gives you $700/month for 96 months:

$700 x 96 = $67,200

After age 70, the difference between the early check and the delayed check is $540/month:

$1,240 - $700 = $540

So the basic breakeven is:

$67,200 / $540 = 124.4 months

That's a little more than 10 years after age 70. In the simple nominal-dollar version, you need to live a little past 80 before the larger delayed check catches up to the eight years of skipped age-62 checks.

That's the conventional breakeven. It's useful, but it leaves out the most important part for a FIRE household.

It treats the skipped age-62 checks as if they simply vanish.